Month: October 2019

2-Factor Authentication: The great switch to Authy from Google Authenticator

After 2 years my Pixel 2 XL took a bit of a spill the other day. Its still fine, but the glass is cracked. I’m hoping to find someone who can change just the glass… but… I bought a Pixel 4 XL. The saddest part about this is I was literally just thinking I would…

The landrush that is naming on the Internet

When I started my company, I registered Github, Linkedin, Twitter, Gitlab, … all the usual suspects. I did this to avoid some unfortunate future situation where I was locked out of a channel I needed. But some of the sites are algorithmic or achievement-unlocking in order to get a custom URL. One example is YouTube.…

Canadian banks still don’t have 2FA. Who are the real criminals here?

In 2014 the Globe and Mail wrote an article called “Why Canada’s banks have weaker passwords than Twitter or Google”. In 2018 I also wrote about this. I opened a support ticket for my bank complaining about this, their response was that “your password plus personal verification question is 2-factor”. E.g. you have 2 passwords,…

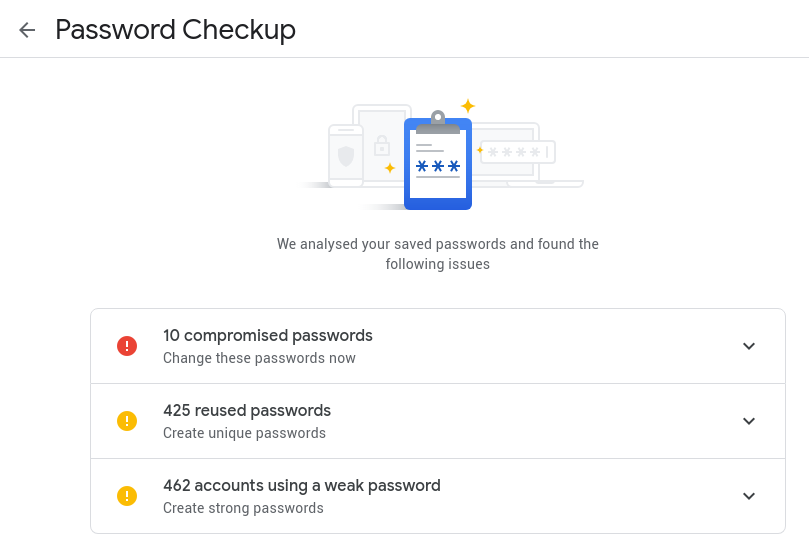

Use chrome? Use passwords? Take 2 minutes and check their value

Head on over to https://passwords.google.com/. This will give u a quick overview of which of your passwords are: compromposed reused weak It runs the check in your browser (in JavaScript) so you are not exposing anything more. Its a cheap simple test (for those who use chrome). Give it a go.